Ontex Sales Fall to $2.08 Billion in 2025 as Baby Care Volumes Weaken

.webp)

Share Post

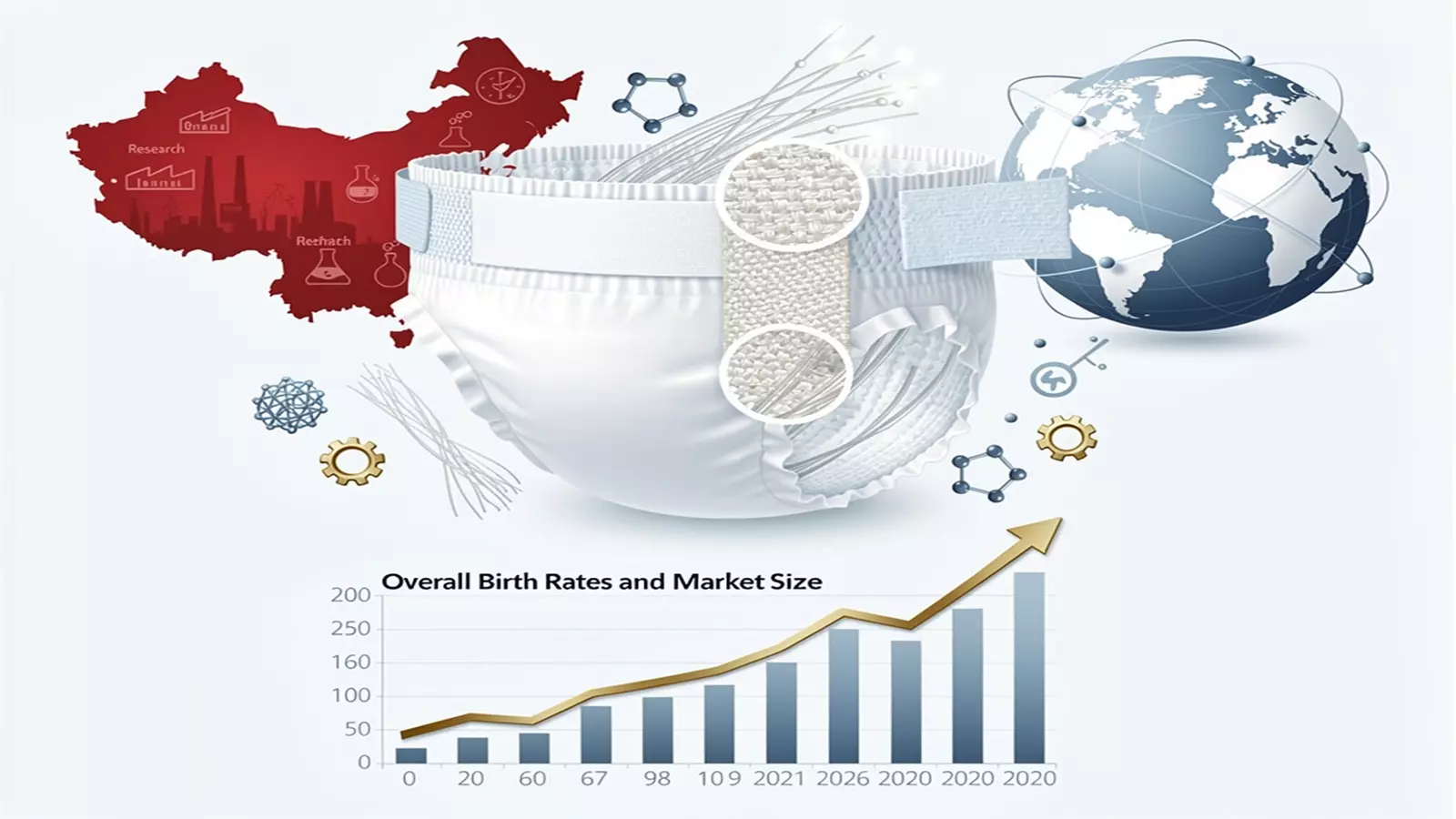

Belgium-based Personal Hygiene major Ontex closed 2025 on a weaker note, reporting a 4.9 percent year-on-year decline in like-for-like revenue to €1.76 billion (approximately $2.08 billion) for the year ended December 31, 2025. The contraction was primarily volume-driven, with overall volumes falling 5 per cent, largely due to continued weakness in the baby care segment. Pricing and product mix had a limited net effect, while foreign exchange movements exerted a marginal 0.4 per cent negative impact.

Profitability also came under pressure during the year. Adjusted EBITDA declined 21 percent to €175.6 million from €222.6 million in 2024, with margins narrowing by 2 percentage points to 10 percent. The impact of lower revenues estimated at around €40 million including reduced fixed cost absorption was compounded by rising input and operating costs. Raw material expenses increased by roughly 4 per cent, driven by higher prices for packaging materials, super-absorbent polymers and fluff pulp. Despite these headwinds, Ontex’s cost transformation programme generated €69 million in net savings, helping offset part of the inflationary burden. Operating profit edged up slightly to €79 million from €75.8 million in the previous year, supported by significantly lower one-off costs.

Segment-wise, Adult Care was the only category to post growth, with revenue rising 1.7 percent to €814.1 million on modest volume gains. Baby Care revenue, however, fell sharply by 12 percent to €696.6 million, reflecting declining birth rates in Europe, subdued consumer confidence and heightened promotional intensity from A-brands. Feminine Care revenue declined 3.6 per cent to €228.2 million, broadly mirroring softer market conditions.

Free cash flow turned negative at €25 million, compared to a positive €48 million in 2024, due to lower EBITDA, higher financing outflows and restructuring expenses. Net financial debt reduced to €577 million following divestments in Brazil and Türkiye, although leverage increased due to weaker earnings.

Looking ahead, the company is targeting around 10 percent adjusted EBITDA growth in 2026, aiming to restore positive free cash flow and gradually reduce leverage as it focuses on tighter execution and operational discipline.

02:25 PM, Feb 18

Other Related Topics

.webp)

China’s Home Interiors Sector Faces Survival Test

10:58 AM, Feb 18

.webp)

Industry Update

1.webp)

1.webp)

1.webp)

1.webp)

1.webp)

1.webp)

1.webp)

1.webp)

1.webp)

1.webp)

1.webp)

1.webp)

1.webp)

1.webp)

1.webp)

.webp)

1.webp)

1.webp)

1.webp)

1.webp)

1.webp)

1.webp)

1.webp)

Kolkata Set to Become Textile Sourcing Hub as YARNEX and TEXINDIA Return in January 2026...view more

1.webp)

1.webp)

1.webp)

1.webp)

1.webp)

1.webp)

1.webp)

1.webp)

1.webp)

1.webp)

1.webp)

1.webp)

1.webp)

1.webp)

India Textile Industry 2025 Review: How US Tariffs Hit Exports, and the Road to Recovery...view more

1.webp)

1.webp)

1.webp)

1.webp)

1.webp)

1.webp)

1.webp)

1.webp)

Europe’s Textile Sector Alarms as Ultra-Fast Fashion Firms Partner With Postal Operators...view more

1.webp)

1.webp)

1.webp)

.webp)

1.webp)

1.webp)

1.webp)

.webp)

1.webp)

1.webp)

1.webp)

Indorama Ventures Pioneers Scalable Bio-Based PET Fibers for a Low-Carbon Textile Future...view more

Carrington Textiles Introduces Defence Stock Range for Faster Access to Military Fabrics...view more

1.webp)

1.webp)

1.webp)

.png)

.jpg)

.jpg)

.jpg)

1.jpeg)